Analyzing Crocs' Q2 Earnings: Is it an Opportunity to Buy Undervalued Shares?

Queue Wolf of Wall Street Legend Donnie Azoff... "Women's Shoesssss!" Or should I say, "Plastic Shoessssssss!"

Disclaimer

The information provided in this essay is solely for general educational and informational purposes. I am not a qualified financial advisor, and my perspectives are solely based on personal research and knowledge as a 19-year-old finance student. I do not hold any certifications or licenses to dispense financial advice, nor am I professionally trained in the field of finance or investment.

While I have made efforts to ensure the accuracy and reliability of the content presented in this essay, I cannot guarantee that all information is entirely up-to-date, complete, or error-free. Please conduct comprehensive research before making any financial decisions.

Crocs Rocks!

Crocs (CROX) reported earnings on Thursday, July 27th, and saw their shares fall roughly 15% after the announcement. The popular footwear manufacturer beat Wall Street’s estimates with the following…

Topline Results

Revenue $1.07B vs. $1.04B estimate 2.88% beat

EPS $3.59 vs. $3.10 estimate 15.81% beat

Paid $299.1M in debt, reducing gross leverage from 2.1x to 1.8x.

Long-term net leverage target of 1.0x to 1.5x.

Crocs Q2 Investor Presentation 2023

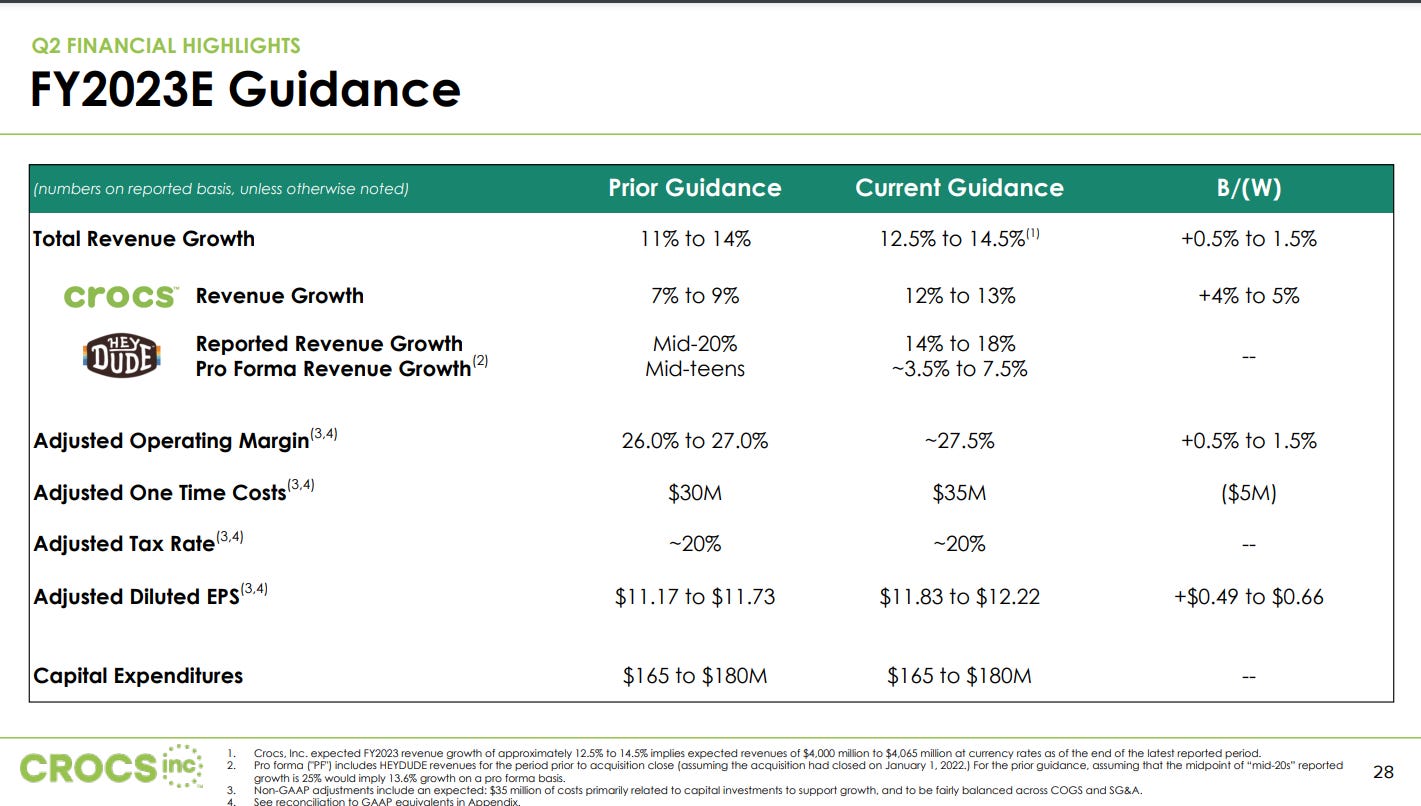

Guidance

Q3 Rev Guidance $1.013-1.034B vs. $1.06B estimate

Q3 EPS Guidance $3.07-$3.15 vs. $3.12 estimate

FY23 Rev Guidance $4.0-$4.065B vs $4.02B estimate

FY23 EPS Guidance $11.83-$12.22 vs. $11.56 estimate

Crocs Q2 Investor Presentation 2023

Buyback

In July 2023, CROX repurchased 0.4 million shares of their common stock for $50.0 million. (~$125/share).

CROX retains $1.0 billion in share repurchase authorization, which can be utilized for potential future repurchases. This would be 15% of the company, as of August 1st.

Crocs Q2 Investor Presentation 2023

What Does Crocs Do?

Crocs is a global footwear company known for its iconic and distinctive clog-style shoes. Founded in 2002, Crocs has gained widespread recognition for its comfortable, lightweight, and versatile footwear. Crocs' signature shoes are made from a proprietary closed-cell resin called Croslite, which offers superior cushioning and durability. Croc’s products come in various styles and colors, catering to a diverse customer base that includes men, women, and children. They can be worn casually around the house or even for light physical activity.

Aside from the classic clogs, Crocs has expanded its product offerings to include various footwear styles, such as sandals, sneakers, boots, and flats. Crocs has managed to create a unique niche in the market, attracting loyal customers who appreciate the brand's distinctive design and comfortable fit.

Crocs Q2 Investor Presentation 2023

In their investor presentation, Crocs emphasizes the significance of their sandals by projecting an impressive 29% revenue growth for this product category in 2023, reaching a substantial $400 million. As a lifestyle brand in the footwear industry, Crocs showcases a captivating range of warm and inviting colors, catering to diverse preferences and ensuring their product offerings suit various consumer needs.

In addition to the Crocs brand, the company owns other footwear labels, such as Jibbitz and HeyDude. Jibbitz are decorative charms that can be attached to the holes on Crocs shoes, allowing customers to customize and personalize their footwear. (Literally a genius idea.) HeyDude was acquired in 2021 for $2.5 billion and specializes in lightweight, comfortable shoes, particularly in the men's and women's casual footwear segments. This acquisition has further expanded Crocs' product portfolio and market reach. It would be nice to see Crocs continue to make acquisitions. While this could be seen as “artificial growth”, I believe it’s more of Crocs building a strong brand that serves a wide customer base.

Crocs Q2 Investor Presentation 2023

By partnering with companies such as Taco Bell & Satisfty, Crocs furthers their customer reach.

Crocs generates its revenue primarily through the sale of its footwear products across various distribution channels. These channels include direct-to-consumer sales through its e-commerce platform and company-owned retail stores, as well as wholesale partnerships with retail stores and distributors worldwide. Crocs is looking to scale down wholesale partnerships and focus on the direct-to-consumer aspect of their business.

Financials

Income Statement

Are you ready to have your socks knocked off? No, like seriously, I’m not kidding. Check out this income statement.

Crocs Q2 Earnings 2023

This is unbelievable. It might be the best income statement improvement I have ever seen. Let’s break this down for the three months ended June 30, year over year.

Starting with the top line, Crocs saw a substantial increase in revenues, growing by 11.17%. This indicates a healthy demand for their products and a successful execution of their sales and marketing strategies.

The cost of sales, on the other hand, decreased by 3.39%. This reduction in costs is favorable as it directly contributed to the significant surge in gross profit, which rose by 24.82%. Crocs has improved its operational efficiency and controlled production expenses.

While revenue is growing fast, SG&A expenses increased by 21.24%. While this could be a cause for concern, it's not unusual for growing companies to invest in sales and marketing efforts to sustain and expand their market share, especially when they are trying to capture foreign market share (an inherently difficult task).

However, the remarkable aspect of Crocs' performance lies in its income from operations, which surged by 28.44%, and EBIT (Earnings Before Interest and Taxes), which grew by 29.45%. These figures demonstrate the company's ability to generate higher profits from its core operations while expanding and growing revenue.

Most impressively, Crocs achieved a net income growth of 32.49%, outpacing its overall revenue growth sizably. This suggests that Crocs not only increased its sales but also managed its expenses efficiently to boost profitability.

Moreover, even on a per-share basis, the diluted net income increased by 31.40%. Although the diluted shares outstanding saw only a nominal rise of 0.49%, it signifies that the increase in net income wasn't merely due to a decrease in the number of outstanding shares but rather genuine income growth, another great sign.

Crocs' income statement improvement for the three months ended June 30 is outstanding. Crocs demonstrated strong revenue growth, effective cost management, and notable profitability expansion. Despite the increase in SG&A expenses, their ability to drive higher income from operations and net income showcases a promising outlook for the company's financial performance. Let’s move on to the balance sheet, where things are just as promising.

Balance Sheet

Crocs Q2 Earnings 2023

Over the period since the end of 2022, Crocs has exhibited some remarkable shifts in its balance sheet. One noteworthy aspect is the 13.2% decrease in cash. While a reduction in cash might seem concerning at first glance, it appears that Crocs has purposefully utilized its cash reserves to address its financial obligations, particularly paying off some of its debt. This strategic move is further corroborated by the significant decline in the debt/asset ratio, which plummeted from 81.90% at the close of 2022 to the current 74.15%. This substantial 7.75% drop in the debt/asset ratio signifies a substantial decrease in the proportion of the company's assets financed through debt. Such a prudent approach indicates a growing commitment to enhancing financial stability and reducing the risk associated with heavy debt burdens.

The 38.57% increase in accounts receivable is a promising sign that Crocs has improved its credit management practices or experienced an upswing in sales with favorable credit terms. The 7.49% decline in inventory shows that Crocs has been successfully managing its inventory levels. By doing so, Crocs can reduce holding costs and enhance overall operational efficiency.

Crocs Q2 Investor Presentation 2023

Inventory decreased 13% y/y, led by a 22.16% decrease in HeyDude & 8.36% decrease in Crocs inventory levels.

It's worth noting that despite the decrease in some current liabilities, total current liabilities rose by 3.85%. This change can be attributed an increase in accounts payable, which grew 13.47%. Overall, Crocs' total assets recorded 2.25% growth, which is fueled by an increase in accounts receivable and prepaid expenses.

Croc’s balance sheet paints a promising picture of the company's financial health and positions it favorably for potential growth and expansion opportunities in the dynamic footwear market.

Note - The cash flow statement, for the most part, encompasses aspects of Croc’s business which I have already touched on. For the sake of time, and length, I will refrain from analyzing it here. You can find it on Croc’s IR website.

Margins

Crocs is an extremely high margin business.

Crocs Q2 Investor Presentation 2023

While HeyDude margins remained flat y/y, Crocs margins increased 410 bps to 62% (insane) and the company as a whole has a 58.1% gross margin.

For reference, Microsoft has a gross margin of ~ 70%, Apple ~50%, Google ~56%.

Here’s the kicker, those are technology companies.

Crocs sells shoes.

Crocs Q2 Investor Presentation 2023

Crocs continues to maintain healthy operating margins with a y/y increase of 20 bps bringing it to an impressive 30.3%. The operating margins for the Crocs brand experienced a significant surge of 350 basis points, reaching 38.4%, indicating the brand's strong performance. However, HeyDude's operating margins saw a noticeable decline of 500 basis points, settling at 27.6%. This drop was a key factor contributing to the decline in the company's stock. The process of scaling up a new acquisition and driving sales through marketing efforts while optimizing costs requires time and cannot be achieved overnight. I’ll touch on this more later.

Geographical Revenue

Croc’s Q2 Earnings 2023

Croc’s has really strong brand recognition in America and is building its moat overseas. In the most recent quarter, not only did Croc’s growth pick up sizably y/y in North America, 12.20%, but growth in the Asia Pacific grew 33.20%! This is absolutely fantastic.

Crocs' popularity in Asian culture is closely aligned with the region's love for unique and quirky fashion trends. In many Asian countries, fashion is seen as a form of self-expression, and people often seek out bold and unconventional styles to make a statement. Crocs' distinctive and comfortable footwear design, along with the wide array of colorful Jibbitz charms, perfectly cater to this desire for individuality and personalization. Jibbitz, which are small, removable charms that can be attached to the holes on Crocs shoes, allow wearers to express their interests, hobbies, and fandoms. This resonates strongly with Asian consumers who embrace the culture of anime and Pokémon, as they can proudly display their favorite characters or symbols on their Crocs, making them a fun and eye-catching accessory.

This is just such a fun company. As Crocs continues to focus on growing in Asia, they can tap into the thriving anime and Pokémon scene in the region. Anime and Pokémon have a massive fan base in Asian countries, with a dedicated community that actively seeks merchandise and products related to their favorite characters and shows. This gives Crocs huge pricing power and a large moat.

Crocs Q2 Investor Presentation 2023

Something to note is that Japan is not even mentioned by Crocs, despite their strong presence there with several brick-and-mortar stores. Regardless, Croc’s growth in Asia is extremely impressive and management expects it to continue.

Additionally, you can see Croc’s presence being felt in China.

HeyDude revenue grew 3% y/y and Croc’s brand revenue grew 13.8% y/y. EMEALA, Europe, Middle East, Africa, and Latin America, revenue was flat, down .20%. I don’t think Croc’s should be targeting revenue growth in those regions as much as they should Asia, for the reasons I have mentioned above. It just fits their culture so well.

I encourage you to read the entire Investor Presentation on Croc’s IR website.

Why Did The Stock Fall?

With an impressive top-line beat and strong fundamentals, the unexpected decline in CROX's stock following its earnings announcement has left many investors surprised.

The primary reason behind CROX's fall can be attributed to weakness in its HeyDude brand. Notably, the wholesale revenue for HeyDude declined by 8.4% y/y, while direct-to-consumer sales experienced a substantial 30 percent increase. Crocs is shifting the HeyDude brand to its online-first strategy, and the issues faced are temporary and not indicative of any permanent impairment to the company's growth trajectory.

Although operating margins for HeyDude also witnessed a noticeable decline of 500 bps y/y, this is largely due to the shift from wholesaling to direct-to-consumer selling, which is expected to result in higher margins in the long run. Considering Crocs' spent $2.5 billion in acquiring HeyDude in 2021, the market's anticipation of HeyDude becoming a significant contributor to Crocs' topline growth is well-founded. Consequently, any weakness in this segment is likely to prompt a reaction in the market.

Management's semi-cautious outlook for wholesale partners can be attributed to various factors, including concerns about overall traffic trends and consumer behavior, excess inventory of other brands, and historical performance trends for HeyDude during the latter half of the year (which have been soft). I’m viewing these challenges as growing pains associated with scaling a shoe brand. Crocs' strong brand recognition and growing global presence more than offset the temporary setbacks faced by HeyDude. The company's resilient moat and expanding market presence worldwide, especially in Asia, suggest that Crocs will continue to do well.

Current Valuation

You can not value Crocs as some legacy shoemarker or a boring business selling a boring product.

Crocs is creating a lifestyle brand and making footwear exciting.

With massive revenue growth, and insanely high margins, Crocs deserves a premium in it’s valuation. However, this is certainly not reflected in the current share price.

With a trailing P/E of ~ 10, FWD P/E of ~ 9, P/S of 1.74 & P/B of 5.61, Crocs is being price like a dinosaur.

I will take advantage of this mispricing.

TLDR Thesis

The recent decline in Crocs' share price following the Q2 earnings release appears to be driven by unrealistic market expectations and temporary issues related to their HeyDude brand and distribution model. Shifting from wholesale to direct-to-consumer takes time, and margins will inevitably be hit. Croc’s solid Asia growth strategy and large lifestyle moat signal a favorable investment opportunity, especially at its current valuation. This is not advice. Thanks for reading and follow me on Twitter @HernyInvests